- UPI

- Visa credit, debit, and prepaid cards

- Mastercard credit, debit, and prepaid cards

- Rupay credit, debit, and prepaid cards

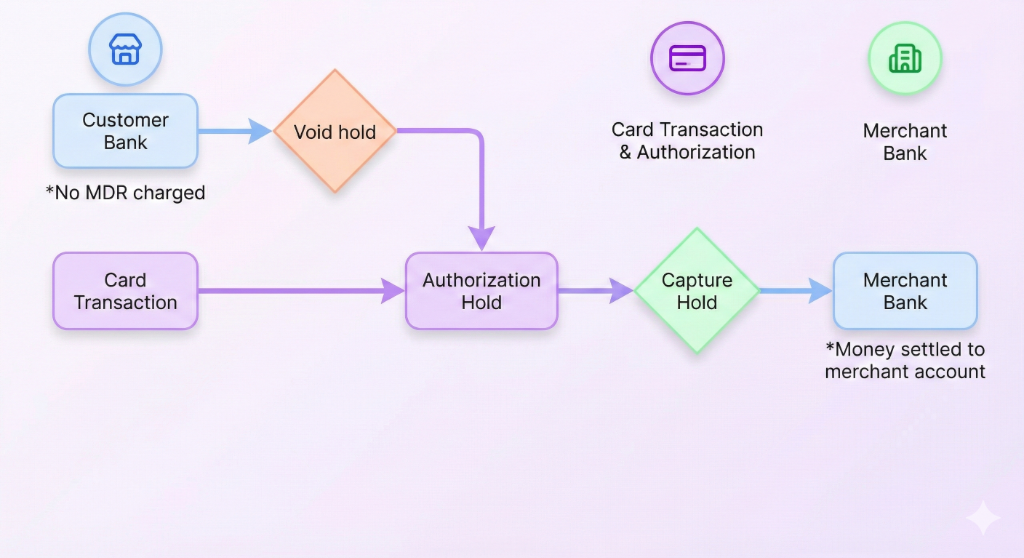

How preauthorisation works

Preauthorisation allows you to manage payments flexibly in the following ways:- Authorise an amount on a customer’s card or account without immediate capture.

- Capture the authorised amount later—either fully or partially—when required.

- Void the authorisation to release the blocked funds if the order is not fulfilled.

Preauthorisation flow

- The customer initiates the payment.

- The bank blocks the amount on the customer’s card or account after successful payment completion.

- You can:

- Either Capture the full or partial amount.

OR - Void the authorisation to release the blocked funds to the customer.

Note: If not captured within seven days, the funds are automatically released.

Preauthorisation feature request

Please use the raise an issue support form to request this feature to be enabled for your account.

Managing preauthorisation transactions

You can capture or void preauthorisation transactions from the Merchant Dashboard or integrate the capture and void APIs to automate the process.Note

- You must capture or void a preauthorisation transaction within seven days of authorisation.

- A transaction can only be captured or voided once.

- Once captured, a transaction cannot be voided.

- Once voided, a transaction cannot be captured.

- Transactions not captured within seven days are automatically released back to the customer.

- Voided transactions return funds to the customer immediately.

- After preauthorisation is enabled for your account, ensure all preauthorisation transactions are either captured or voided.

- For UPI, you can capture the transaction for up to one year or until the expiry date, whichever occurs first.

Supported payment instruments for preauthorisation

Cashfree Payment Gateway supports preauthorisation workflow on cards and UPI (Unified Payments Interface).Cards

Once preauthorisation is enabled for your account, every card payment will be preauthorised by default, you do not need to provide any additional parameters while initiating the payment. Below is a sample Order Pay API request and response:UPI

For UPI preauthorisation, you need to pass additional parameters in the/orders/pay API request. Once you have created the order, invoke the Order Pay API call with the authorize_only, authorization parameters.

The authorization object contains the following attributes:

approve_by- The time by when customer needs to approve this one time mandate request.start_time- The time when the mandate should start.end_time- The time until when the mandate hold will be on customer’s bank account. You can call capture and void until this time.

UPI collect

Below is a sample UPI Collect request and response:UPI intent

Below is a sample UPI Intent request and response:Capture

The capture workflow helps you to capture the payment and move the authorised amount partially or completely from customers bank account to your bank account, by calling Preauthorisation API for capture.Void

The void workflow helps you to release the entire authorised amount back to the customer, by calling Preauthorisation API for void.FAQs

What is the validity of capture?

What is the validity of capture?

If not captured within 7 days, the authorisation expires, and the funds are released back to the customer.

Can a merchant capture a partial amount?

Can a merchant capture a partial amount?

Yes, merchants can capture a partial amount of the authorised funds.

Can a merchant void a partial amount?

Can a merchant void a partial amount?

No, voiding must be for the entire authorised amount.

What happens if a customer disputes a settled transaction?

What happens if a customer disputes a settled transaction?

A dispute may result in a chargeback, requiring the merchant to provide proof of authorisation and service fulfilment.